Ah, la caution solidaire bancaire... and la liquidation judiciaire. Sounds intimidating, doesn't it? Like something you'd only hear whispered in hushed tones by lawyers. But let's demystify it, shall we? Imagine you're starting a small business. You're brimming with enthusiasm, right?

You need a loan from the bank. Easy enough, you think! But the bank, being, well, a bank, wants guarantees. They want to make absolutely sure they get their money back. That's where the caution solidaire bancaire might come into play.

What exactly is it? Simply put, it's someone (or several someones!) agreeing to pay back the loan if you, the business owner, can't. Think of it as a safety net. A pretty serious one, though!

This "someone" is the caution. Usually, it’s a family member, a close friend, or even another business partner. They’re essentially saying, "I trust this person and this business, and I'm willing to put my own assets on the line." Big commitment, isn't it?

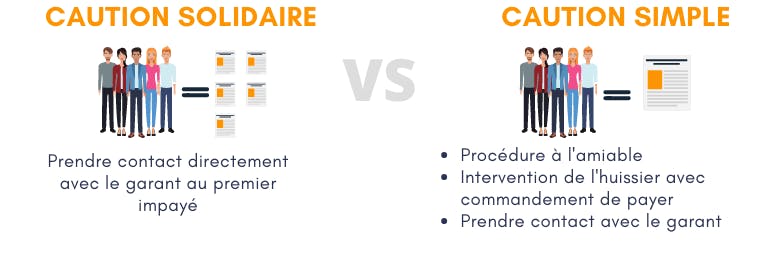

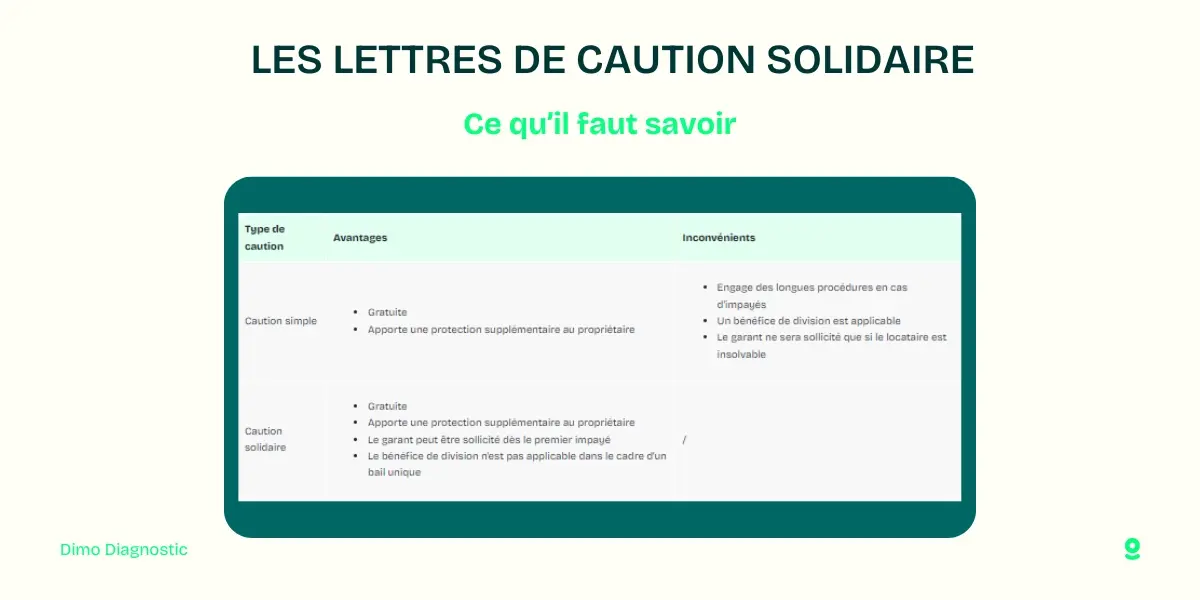

But what does "solidaire" mean? It means they're jointly and severally liable. In simpler terms, the bank can come after the caution for the entire debt, even if there are other guarantors. Yes, the entire debt! Scary stuff, huh?

Now, let’s imagine things don't go as planned. Business is tough. The market shifts. Unexpected expenses pop up. Suddenly, you find yourself struggling to keep up with the loan repayments. This is where the dreaded liquidation judiciaire enters the picture.

Liquidation judiciaire? It's essentially bankruptcy for a company. The business can no longer pay its debts. The court appoints a liquidator, who sells off all the company's assets to try and pay back creditors.

So, what happens to the caution solidaire when a liquidation judiciaire occurs? Well, that's where the situation gets, shall we say, uncomfortable.

The bank, having exhausted its options with the now-bankrupt company, will likely turn to the caution. Remember that safety net? It’s about to be put to the test.

The bank will send a formal demand for payment to the caution. This demand outlines the amount owed, including principal, interest, and any other applicable fees. It's not a friendly letter, trust me.

The caution now has a decision to make. Can they pay the debt? If they can, they might try to negotiate a payment plan with the bank. It's worth a shot, right?

But what if they can't pay? What if the amount owed is simply too large? This is where things get tricky, and often require serious legal advice.

There are a few potential defenses the caution might explore. Did the bank fail to provide adequate information about the business's financial situation before the guarantee was signed? Was the guarantee disproportionate to the caution's assets and income?

These are complex legal questions, and the answers can depend heavily on the specific circumstances. That’s why consulting with a lawyer specializing in banking law and bankruptcy is absolutely crucial.

Think of it this way: you wouldn't try to fix a car engine without a mechanic, would you? Similarly, navigating the legal complexities of a caution solidaire and a liquidation judiciaire requires professional expertise.

Let's delve a little deeper into these potential defenses. The "disproportion" argument is a common one. The law protects individuals from taking on guarantees that are clearly beyond their means. Imagine someone with a modest income guaranteeing a multi-million euro loan. That's likely to be considered disproportionate.

However, the courts will look at a variety of factors, including the caution's assets, income, and overall financial situation. It's not a simple calculation; it's a holistic assessment.

Another potential defense involves the bank's duty to inform. Banks have a responsibility to provide potential cautions with accurate and complete information about the risks involved. Did the bank disclose the true financial health of the business? Did they downplay the risks involved?

If the bank failed to fulfill this duty, the caution might have grounds to challenge the validity of the guarantee. Again, this is where legal expertise is essential. Proving that the bank withheld information can be challenging, but it's not impossible.

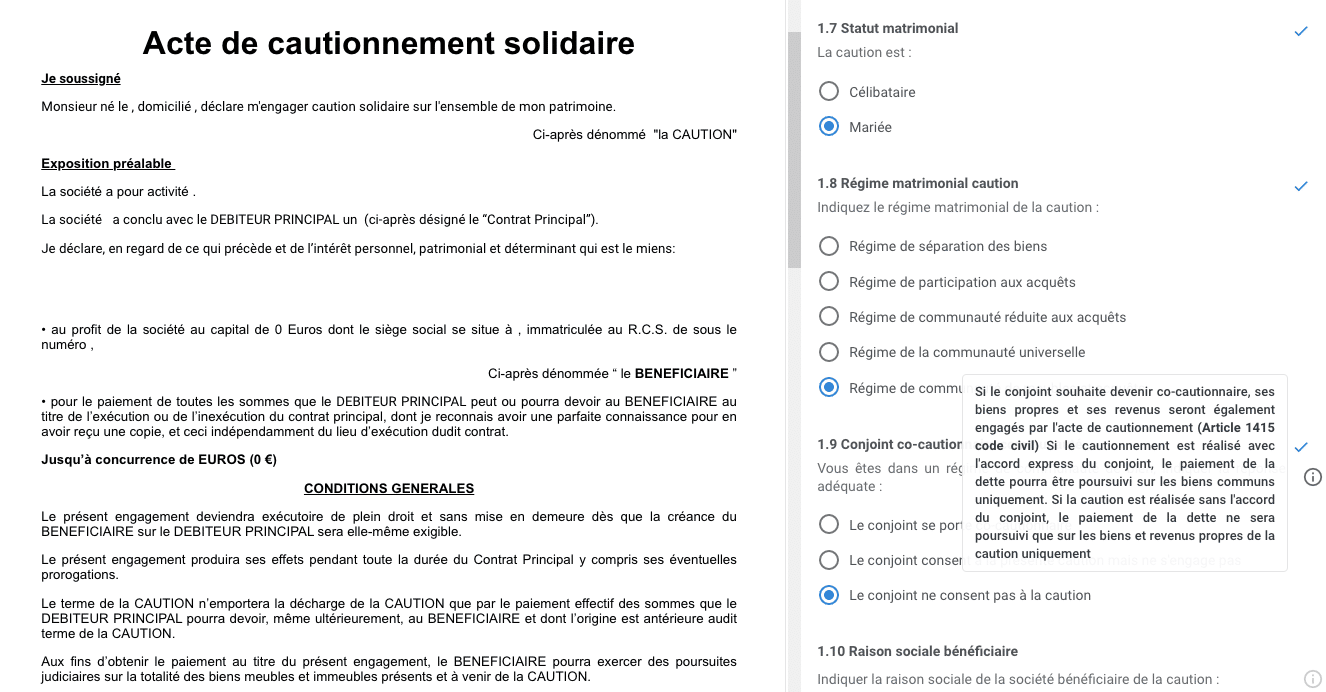

What if the caution is married? In France, the marital regime can significantly impact the enforceability of a guarantee. If the guarantee was signed without the consent of the spouse, it might be unenforceable, especially if the couple is married under a community property regime.

These are just a few of the potential legal avenues that a caution might explore. The key takeaway is that a liquidation judiciaire doesn't automatically mean the caution is doomed. There are often options available, but they require careful consideration and expert legal guidance.

And what happens if the caution is themselves declared bankrupt? Well, then their assets are also subject to liquidation. It's a cascading effect, highlighting the serious risks involved in providing a guarantee.

The best advice? Think very, very carefully before agreeing to be a caution solidaire. Understand the risks involved. Get independent legal advice. Don't let enthusiasm or friendship cloud your judgment.

Before signing anything, ask yourself: Can I really afford to pay back this loan if the business fails? If the answer is anything less than a resounding "yes," proceed with extreme caution. La prudence est mère de sûreté, as they say!

And remember, there are other ways to support a friend or family member starting a business. You can offer advice, mentorship, or even a small loan that you're prepared to lose. These options are often less risky than providing a formal guarantee.

So, what's the takeaway from all this? La caution solidaire bancaire and la liquidation judiciaire are serious matters with significant consequences. Knowledge is power. By understanding the risks and seeking expert advice, you can protect yourself and make informed decisions.

It's a complex world, business, law, all of it. But with a little understanding, and a lot of careful thought, you can navigate it all. Remember, even in the darkest of times, there is always hope. Always the possibility of a fresh start. Perhaps a new venture, perhaps a new way of looking at things. Courage!

And you know what? Sometimes, even when things look bleak, a little kindness can go a long way. Maybe that's the most important lesson of all. Offer a helping hand. Lend an ear. Be there for someone who's struggling. Because at the end of the day, we're all in this together. Isn’t that a comforting thought?

![[Droit bancaire] Comment annuler une caution bancaire solidaire ? Nos](https://amauryayoun.com/wp-content/uploads/2023/08/capture-decran-2023-08-26-a-19.44.56.png)