Okay, mes amis, pull up a chair, grab a café au lait (or maybe something a little stronger, depending on how your investments are doing!), because we need to talk about something wildly exciting…taxation! I know, I know, sounds thrilling as watching paint dry, right? But stick with me, because we're diving into the wonderfully wacky world of the Prélèvement Forfaitaire Non Libératoire, specifically as it applies to assurance vie.

Think of me as your slightly-caffeinated, definitely-not-an-accountant tour guide through this bureaucratic jungle. We’ll try to keep it light, promise! After all, taxes are serious business, but that doesn’t mean we can’t have a chuckle along the way. Imagine trying to explain this to your average baguette-wielding Frenchman - the confused shrug would be legendary!

So, what is this 'Prélèvement Forfaitaire Non Libératoire' beast?

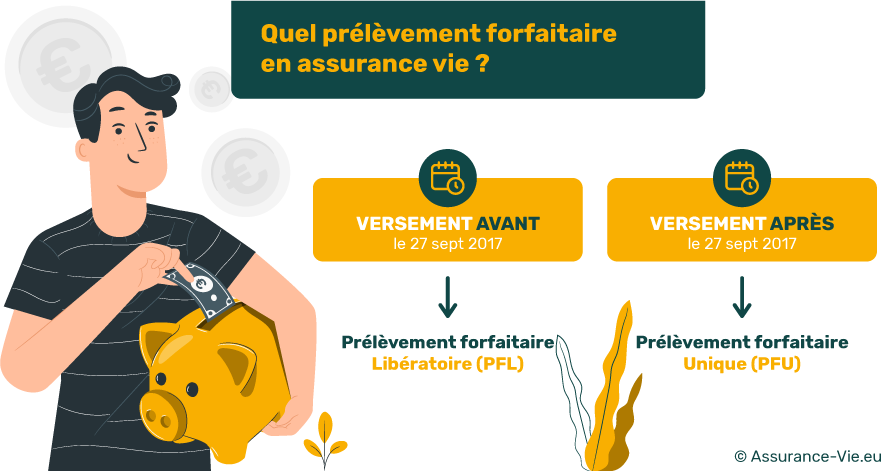

Right, let's break it down. "Prélèvement" means "deduction." "Forfaitaire" means "flat-rate." "Non Libératoire" means... well, let's just say it means it’s not the final word on your tax obligations. Think of it as a down payment on your taxes, a little something the government snags upfront. It's basically saying, "Hey, we know you're making money. Give us a little taste, and we'll sort out the details later." Sounds fair, doesn't it? (Insert maniacal laughter here).

Now, specifically, we're talking about how this applies to your assurance vie, which, as you probably know, is a life insurance policy that also acts as a savings and investment vehicle. It's like a Swiss Army knife for your finances! You can save for retirement, a down payment on a château, or even just a really, really nice vacation. And, of course, like anything that makes you money, the government wants a piece of the action.

The "Non Libératoire" bit – Decoding the Confusion

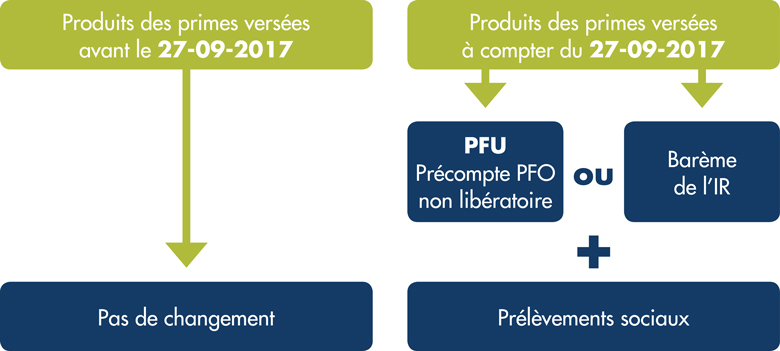

The Non Libératoire part is crucial, and probably the most confusing. It means that this initial deduction isn't the end of the story. When you file your annual income tax return, the tax authorities will recalculate your taxes based on your overall income and applicable tax brackets. This initial deduction might then be credited against your final tax liability. Or, brace yourselves, you might owe more! It all depends on your individual situation.

Imagine it like this: you order a pizza and give the delivery guy a €5 tip upfront. But then, when you actually pay for the pizza, it turns out you owed €3 more than you thought! That's the Non Libératoire experience in a nutshell. A bit annoying, perhaps, but at least you got pizza. And, hopefully, your assurance vie is performing better than the delivery guy’s driving!

How Does It Work, Exactly? (With as little math as possible, I promise!)

Okay, here's the gist: When you make a partial or total withdrawal from your assurance vie policy, the financial institution (your bank or insurance company) will automatically deduct the Prélèvement Forfaitaire Non Libératoire from the taxable portion of your withdrawal.

Here's a simplified breakdown:

- You make a withdrawal: Let's say you decide to withdraw some funds from your assurance vie. Good for you! Maybe you're buying a yacht. Or, you know, just paying the electricity bill.

- The taxable portion is calculated: Not all of your withdrawal is taxable! Only the "gain" (the difference between what you initially invested and what the policy is now worth) is subject to this deduction. Think of it like this: you planted a tiny seed and it grew into a money tree. The government only wants a cut of the fruit (the gain), not the soil and water (your initial investment).

- The Prélèvement Forfaitaire Non Libératoire is applied: The bank applies the flat-rate tax to this gain. The exact rate depends on how long you've held the policy. More on that later!

- You receive the rest: You get the remaining amount, minus the deduction. Go forth and spend (or, you know, save responsibly)!

- Come tax season: You declare your assurance vie withdrawals on your income tax return. The tax authorities will then recalculate your taxes and credit you for the Prélèvement Forfaitaire Non Libératoire you already paid.

It's basically a game of financial peek-a-boo with the taxman. He takes a little bit now, and then you see if you get it back (or owe more) later. Fun, right?

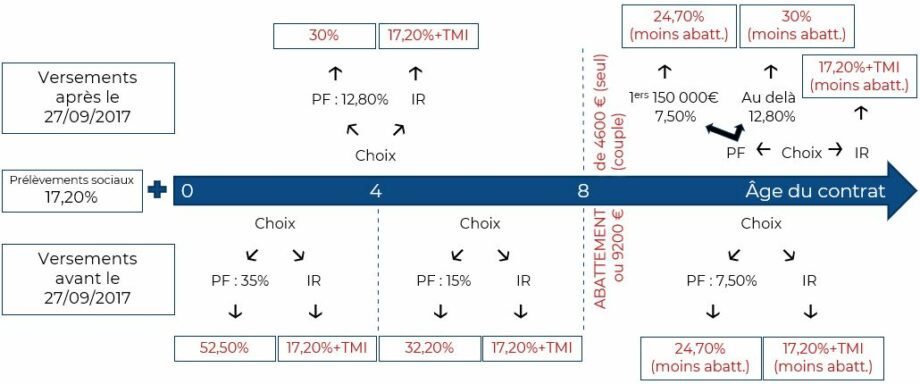

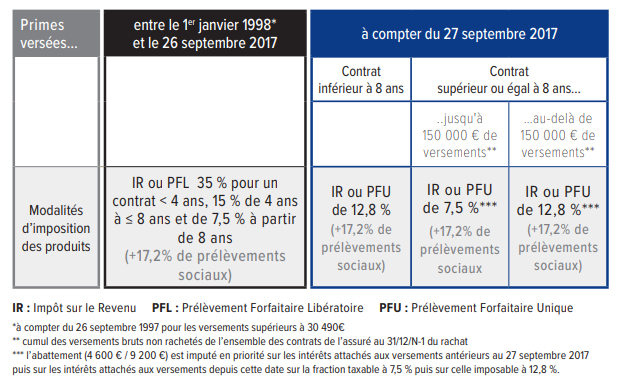

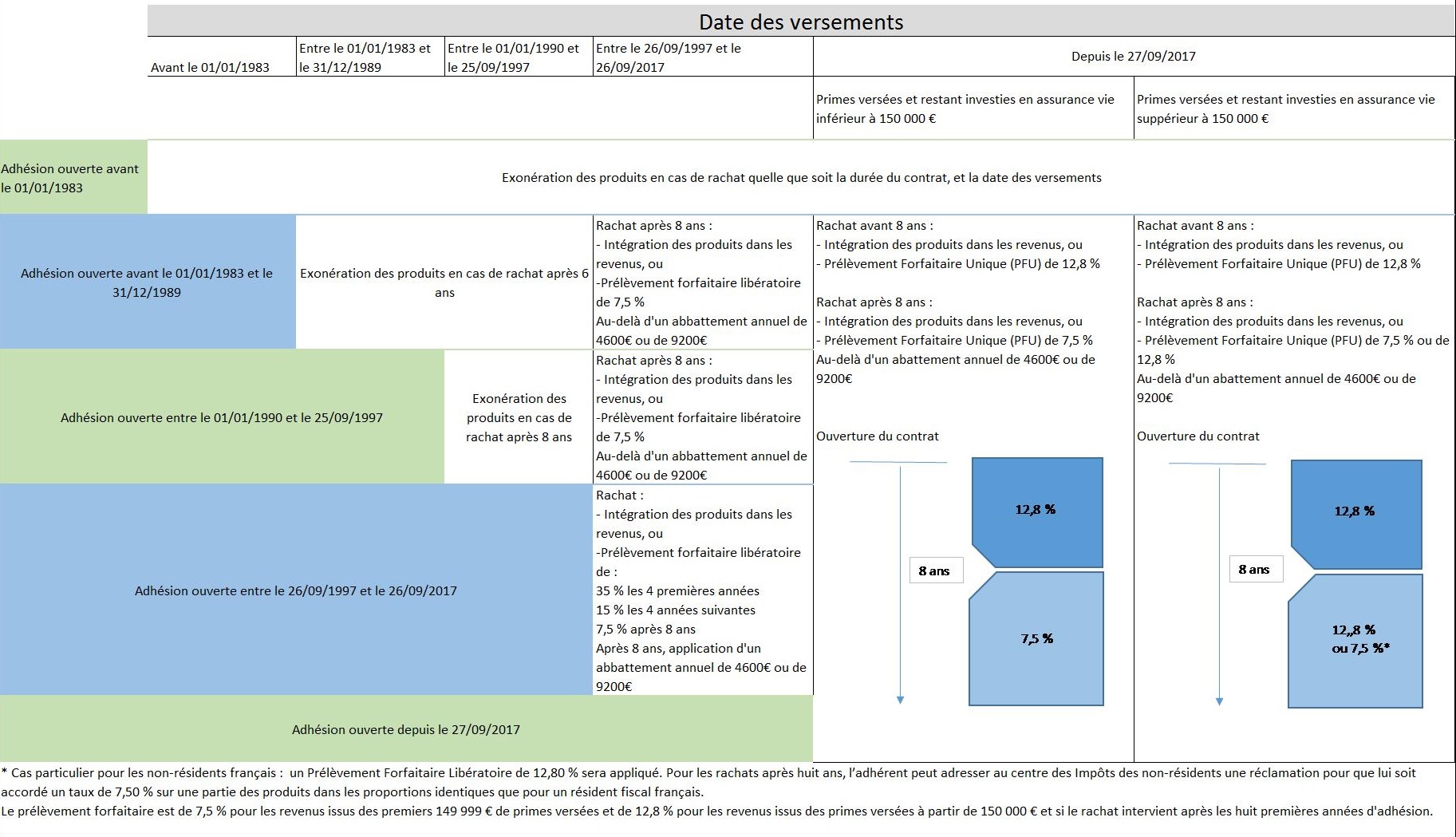

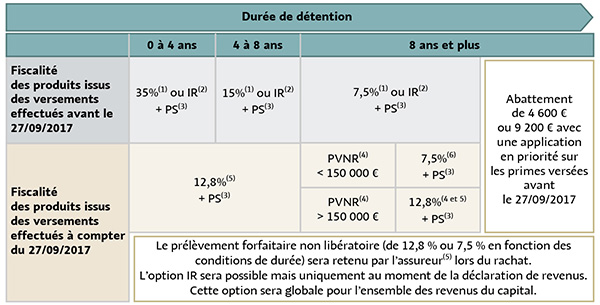

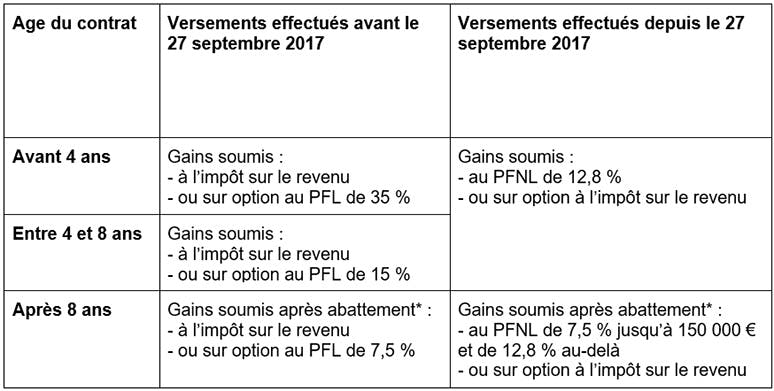

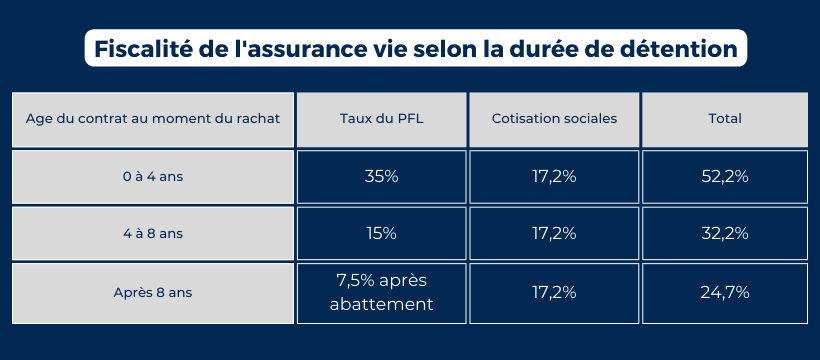

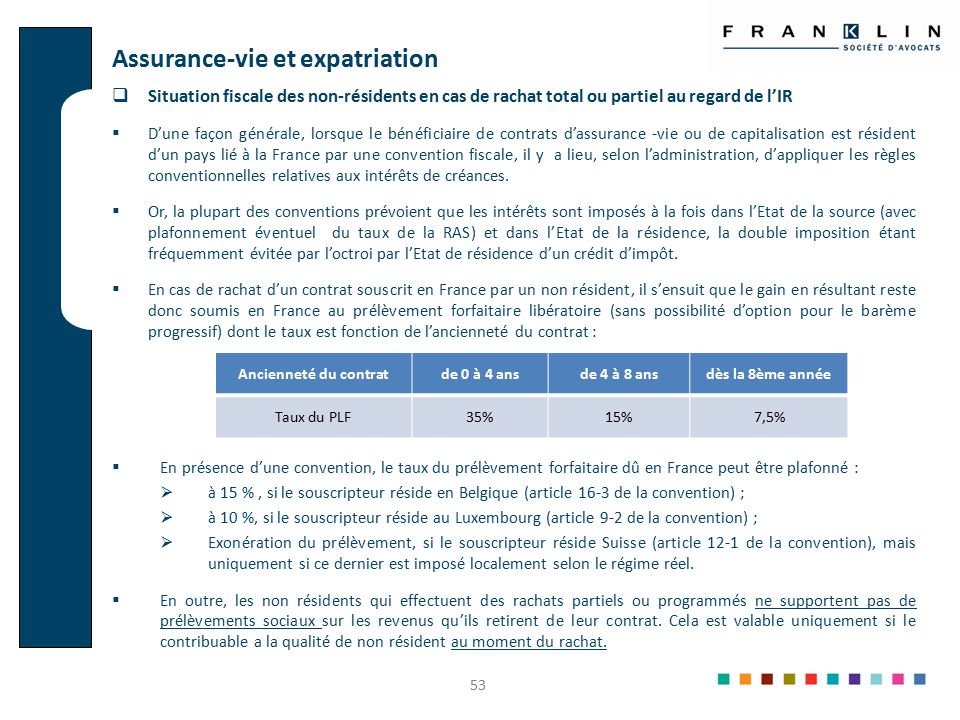

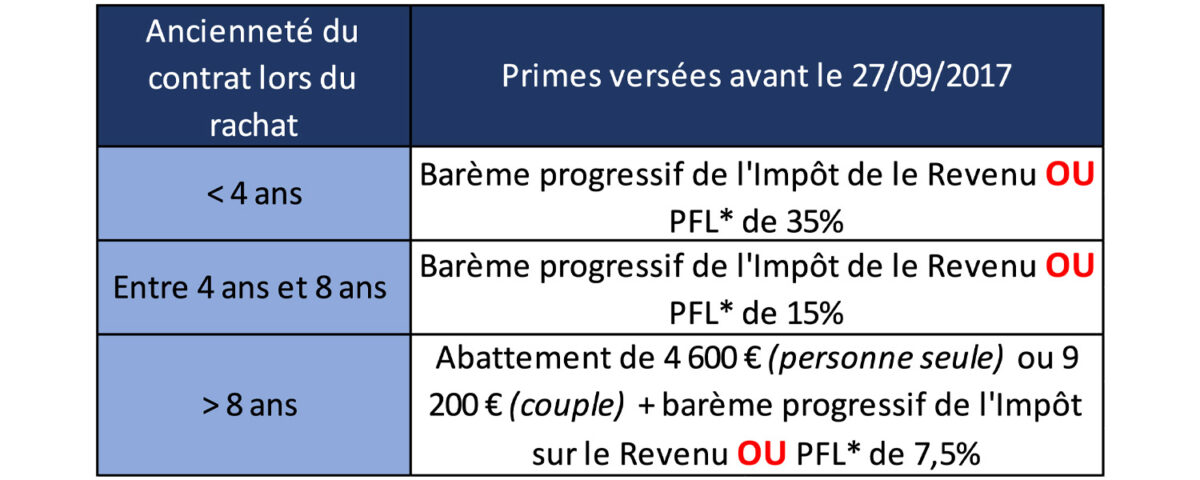

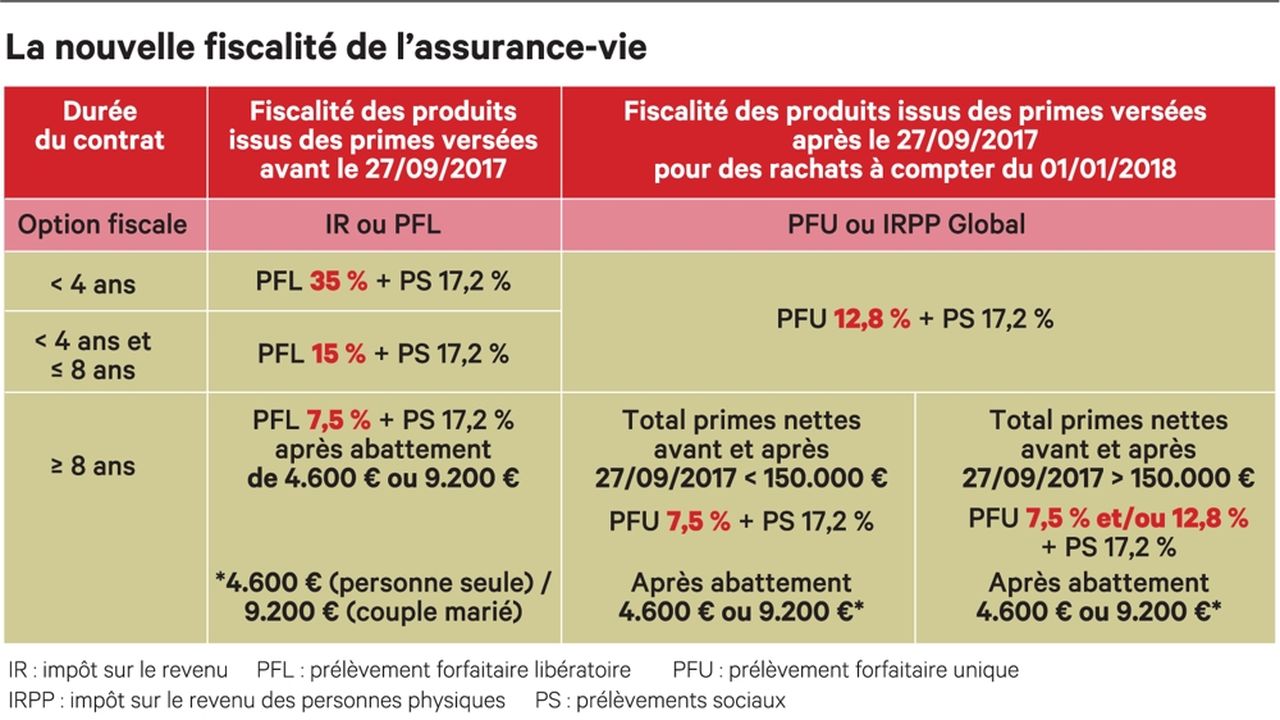

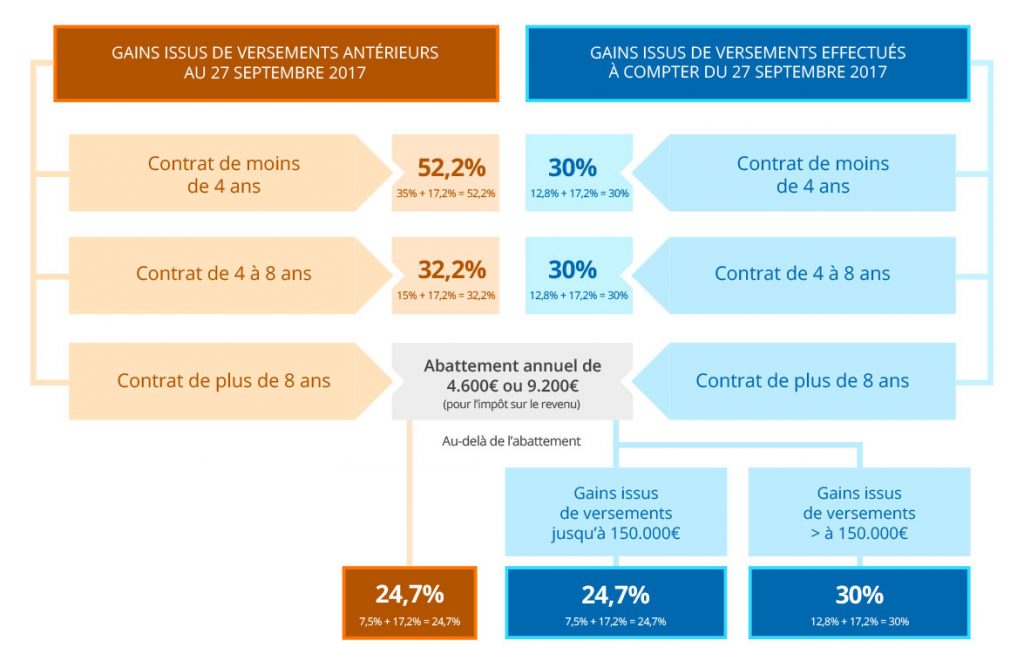

The Rates – Because Numbers are Inevitable

Alright, we can't avoid them completely. The rates for the Prélèvement Forfaitaire Non Libératoire depend on how long you've held the assurance vie policy:

- Policies held for less than 4 years: The rate is 35%. Ouch! It pays to be patient. Think of it as a penalty for financial impatience.

- Policies held for between 4 and 8 years: The rate drops to 15%. Much better! Now we're talking. This is the sweet spot for many investors.

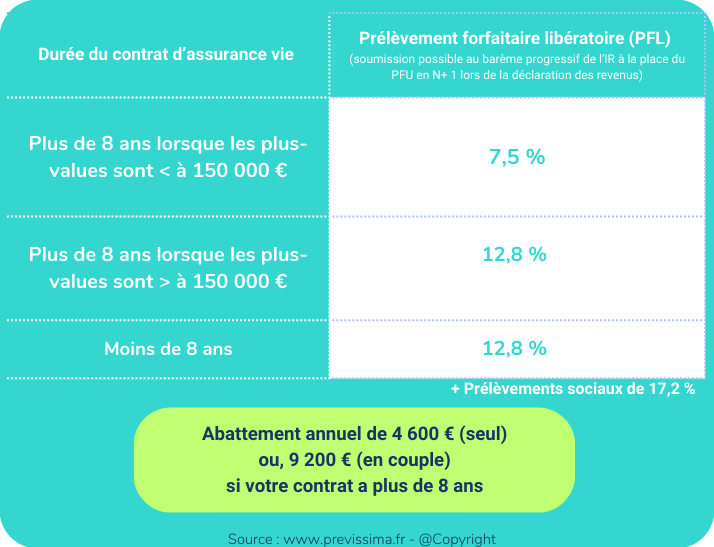

- Policies held for 8 years or more: This is where things get interesting! You usually get to choose between the Prélèvement Forfaitaire Libératoire (PFL) at a rate of 7.5% or having your gains taxed at your marginal income tax rate. And, you get an annual allowance (abattement) on the gains, which can significantly reduce your tax burden. This is where the assurance vie really shines. Like a fine wine, it gets better with age!

Important Note: These rates are for illustrative purposes and can change. Always check with a qualified financial advisor or the French tax authorities for the most up-to-date information. I'm just a friendly voice at a digital café, not a substitute for professional advice!

Why Does This Prélèvement Forfaitaire Non Libératoire Exist?

Ah, the million-euro question! Why does the government do anything? Well, the official explanation is that it simplifies tax collection. It's easier for the government to get a little something upfront than to wait for everyone to file their taxes. It also helps to ensure that people don't avoid paying taxes on their assurance vie gains altogether. Think of it as preemptive tax strike!

The cynical explanation? Well, let's just say governments like money. A lot. And they're very good at finding creative ways to get it. But hey, at least they (presumably) use it to build roads, schools, and, you know, keep the lights on. (Although, sometimes you wonder where all that money actually goes…)

What Should You Do About It?

Don't panic! The Prélèvement Forfaitaire Non Libératoire is a manageable part of the assurance vie landscape. Here are a few tips:

- Plan your withdrawals carefully: If possible, try to avoid making withdrawals from your assurance vie policy in the first four years, as the 35% rate is pretty steep. Patience, mes amis, patience!

- Consider holding your policy for 8 years or more: The tax advantages for long-term assurance vie policies are significant. Think of it as planting a tree – it takes time to grow, but the shade (and the tax benefits) are worth it in the end.

- Keep accurate records: Make sure you keep track of all your assurance vie transactions, including withdrawals and the amount of Prélèvement Forfaitaire Non Libératoire deducted. This will make filing your taxes much easier.

- Seek professional advice: This is the most important tip! Consult with a qualified financial advisor who can help you understand your specific tax situation and develop a plan that's right for you. Don't try to navigate this complex world alone.

In conclusion, the Prélèvement Forfaitaire Non Libératoire is a quirky little piece of the French tax system that you need to understand if you have an assurance vie policy. It's not the end of the world, but it's important to be aware of it and plan accordingly. And remember, a little bit of knowledge (and a good financial advisor) can go a long way!

Now, if you'll excuse me, I think I need another café au lait. And maybe a pain au chocolat. All this talk of taxes has given me a craving for something sweet. À bientôt!