Okay, picture this: my Aunt Ginette, God rest her soul, was a legend at keeping secrets. Turns out, after she passed, we discovered she had this tiny obsession with life insurance policies. I mean, plural. Policies. Suddenly, us cousins were staring down the barrel of paperwork so thick, you could probably build a small fort out of it. And somewhere in that mountain of legal jargon, the phrase "Déclaration Partielle de Succession Pour Assurance Vie" popped up. Cue collective familial blank stares. Seriously, what even IS that?

Turns out, it's less scary than it sounds, but definitely something you need to understand if you're ever in a similar situation. Let's break it down, shall we? Because nobody wants to build a fort out of inheritance paperwork. Trust me.

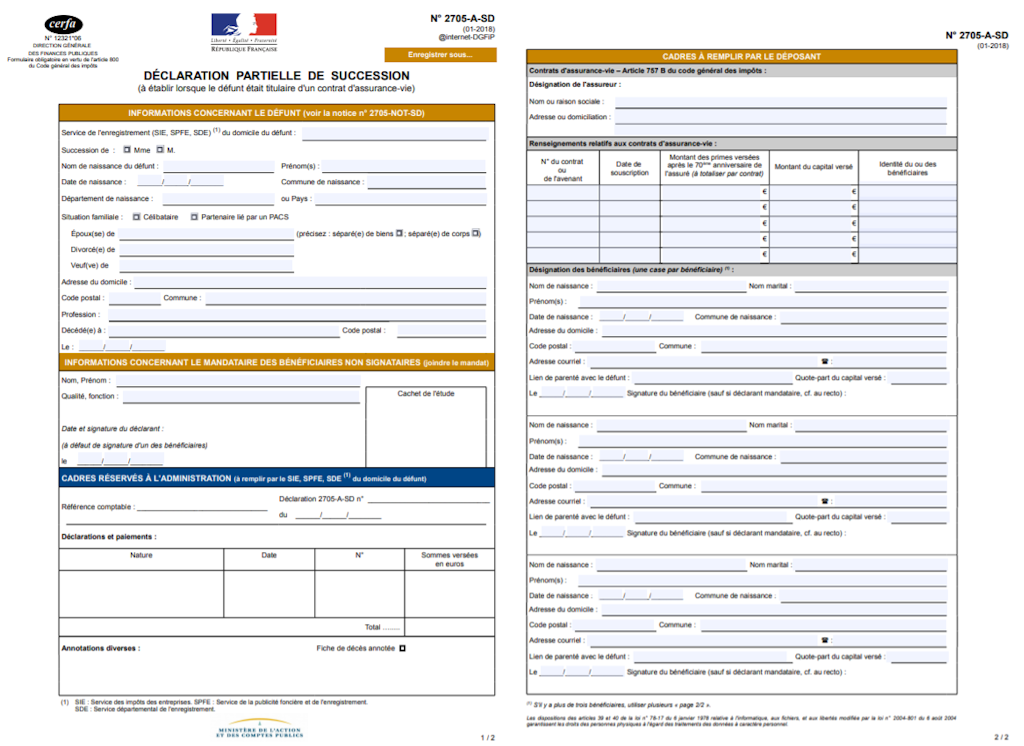

What is a "Déclaration Partielle de Succession Pour Assurance Vie"?

Essentially, it's a partial declaration of inheritance specifically for life insurance policies. Think of it as a mini-inheritance declaration, focused solely on the money from those policies. Why not just include it in the main inheritance declaration? Good question! (I like the way you think.)

The thing is, life insurance money often has its own special set of rules, particularly when it comes to taxes. So, the French tax authorities (l'administration fiscale, for those of you who want to impress your notary) want a clear, separate record of these amounts.

Key takeaway: It's a specific declaration, separate from the general inheritance declaration, focusing on life insurance policy payouts.

Why is it "Partial"?

The "partial" part is important. It emphasizes that this declaration only covers the assurance vie payouts. It doesn’t include Aunt Ginette's antique thimble collection or her questionable taste in ceramic cats (sorry, Aunt Ginette!). It's just about the life insurance money and how it's divided among the beneficiaries.

Think of it like ordering à la carte instead of the whole menu. You're only picking out one specific item.

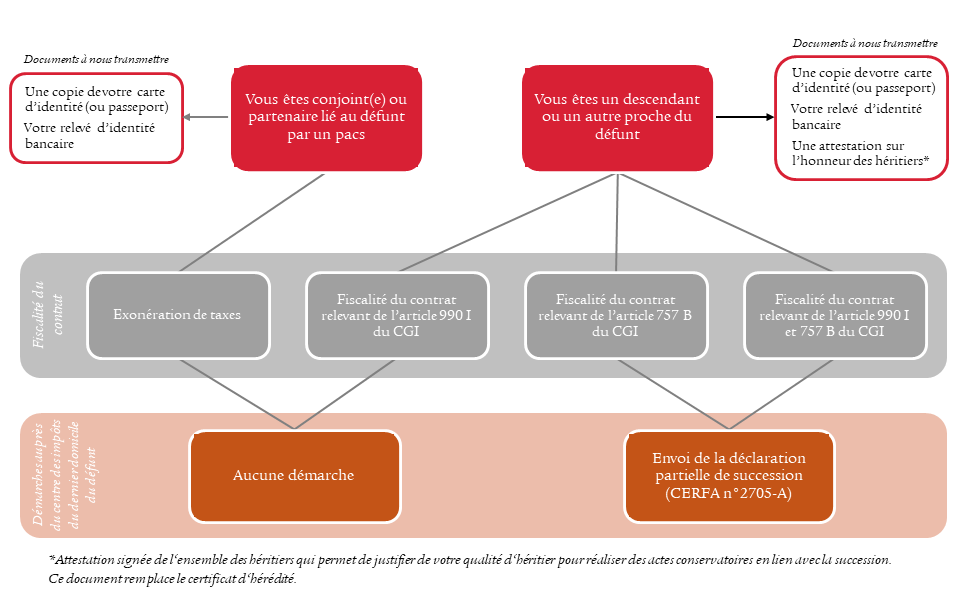

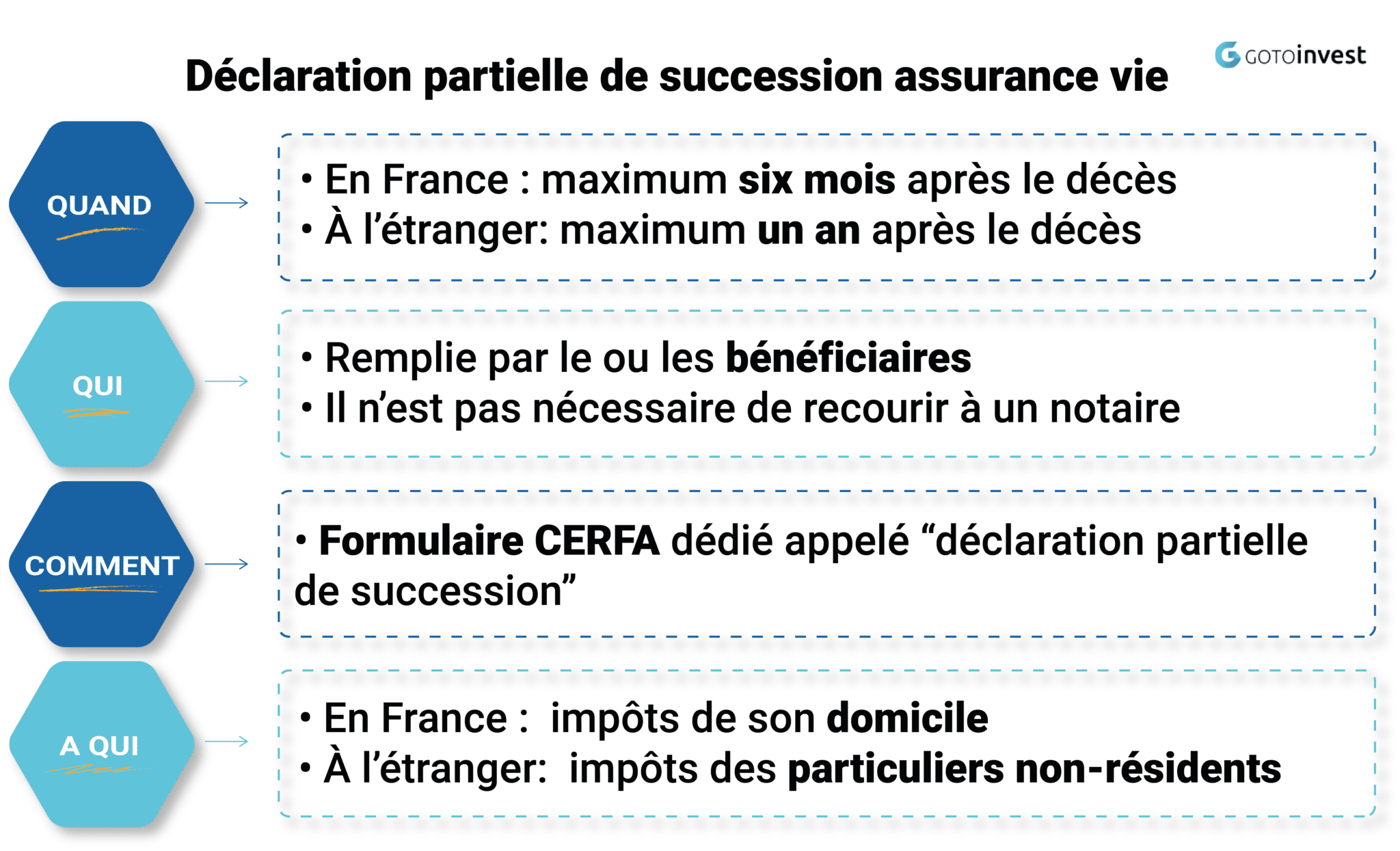

Who Needs to File This Thing?

Generally, it's the heirs or the beneficiaries of the life insurance policies who are responsible for filing this declaration. In practical terms, it usually falls to the person handling the estate (the notaire, the executor, or a designated heir). But even if someone else is doing the heavy lifting, it's good to understand the basics. Just in case, you know?

Side note: If you’re a beneficiary of a life insurance policy, you'll likely be contacted by the insurance company asking for certain documents and information. This might include the "Déclaration Partielle de Succession." So, be prepared!

What Information Do You Need?

Gathering the right information is half the battle. Here’s what you’ll typically need:

- Information about the deceased (the policyholder): Name, date of birth, date of death, address, etc. Basically, all the standard stuff you'd expect.

- Information about the life insurance policy(ies): Policy number, name of the insurance company, amount of the payout, the date the policy was taken out.

- Information about the beneficiaries: Names, addresses, dates of birth, and their relationship to the deceased. Oh, and their social security numbers (numéro de sécurité sociale). Because, France.

- Details of any exemptions or deductions: This is where things can get a little tricky. There are certain exemptions and deductions that might apply to life insurance payouts, which can reduce the amount of inheritance tax owed. (More on that later.)

- Proof of identity and address for all beneficiaries. Photocopies of ID cards and utility bills are your friends.

Pro Tip: Keep copies of everything! Seriously, EVERYTHING. You'll thank me later.

Taxes, Taxes, and More Taxes (Ugh!)

Ah, yes. The dreaded T-word. Life insurance payouts in France are subject to inheritance tax (droits de succession), but there are some exemptions and allowances that can significantly reduce the amount of tax owed.

The amount of tax depends on several factors, including:

- The relationship between the deceased and the beneficiary: Spouses and close family members generally get more generous allowances.

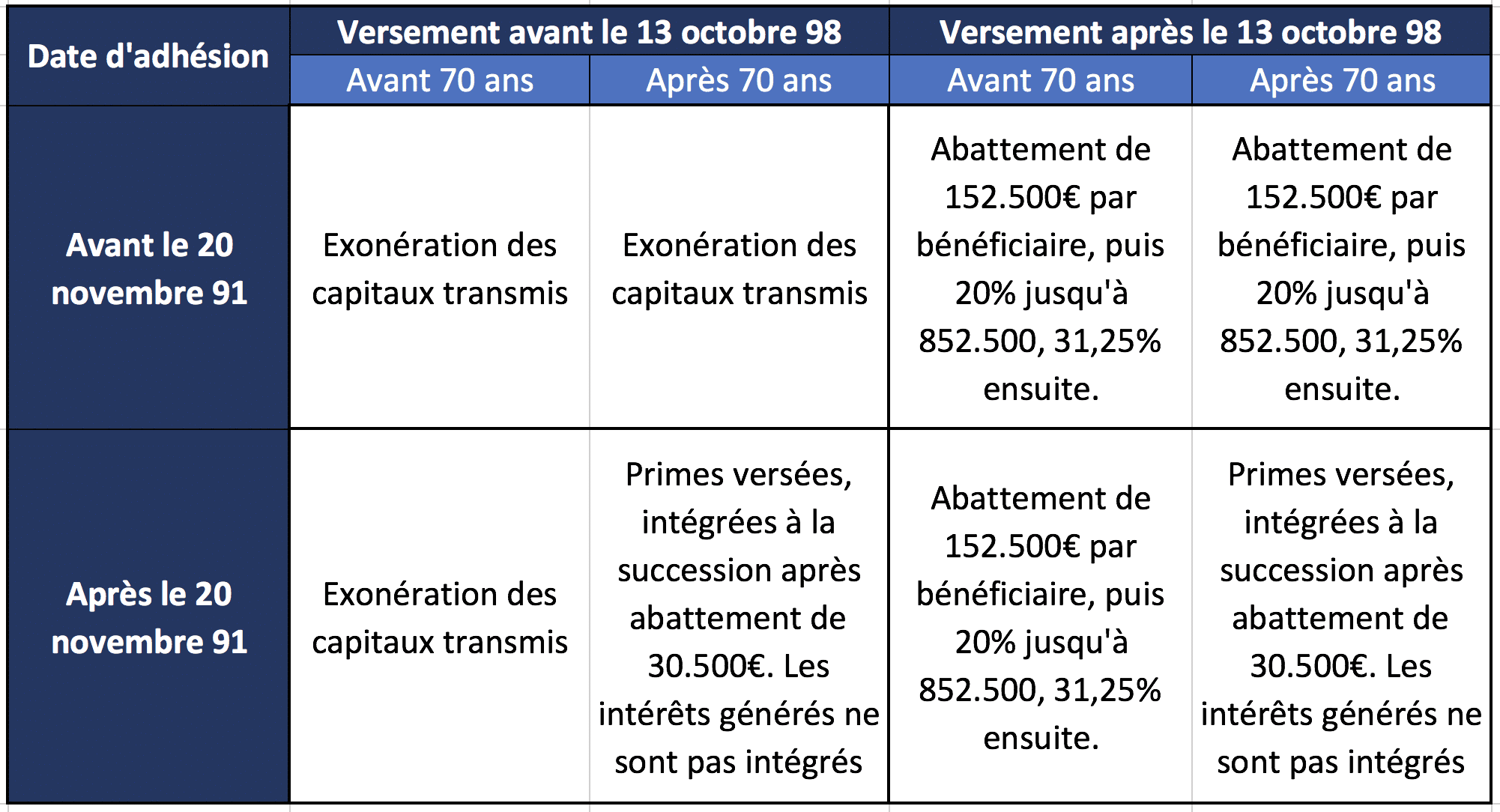

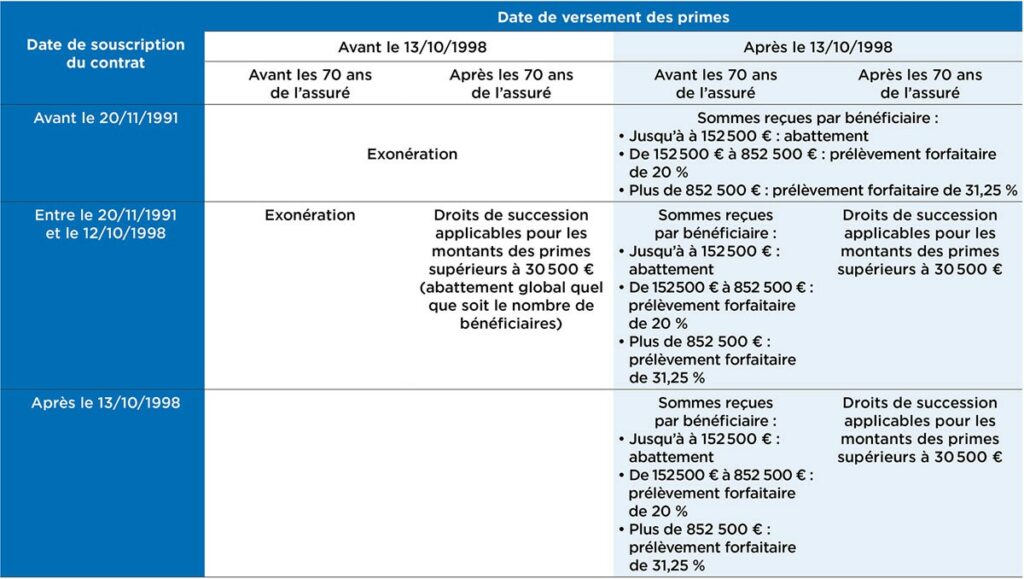

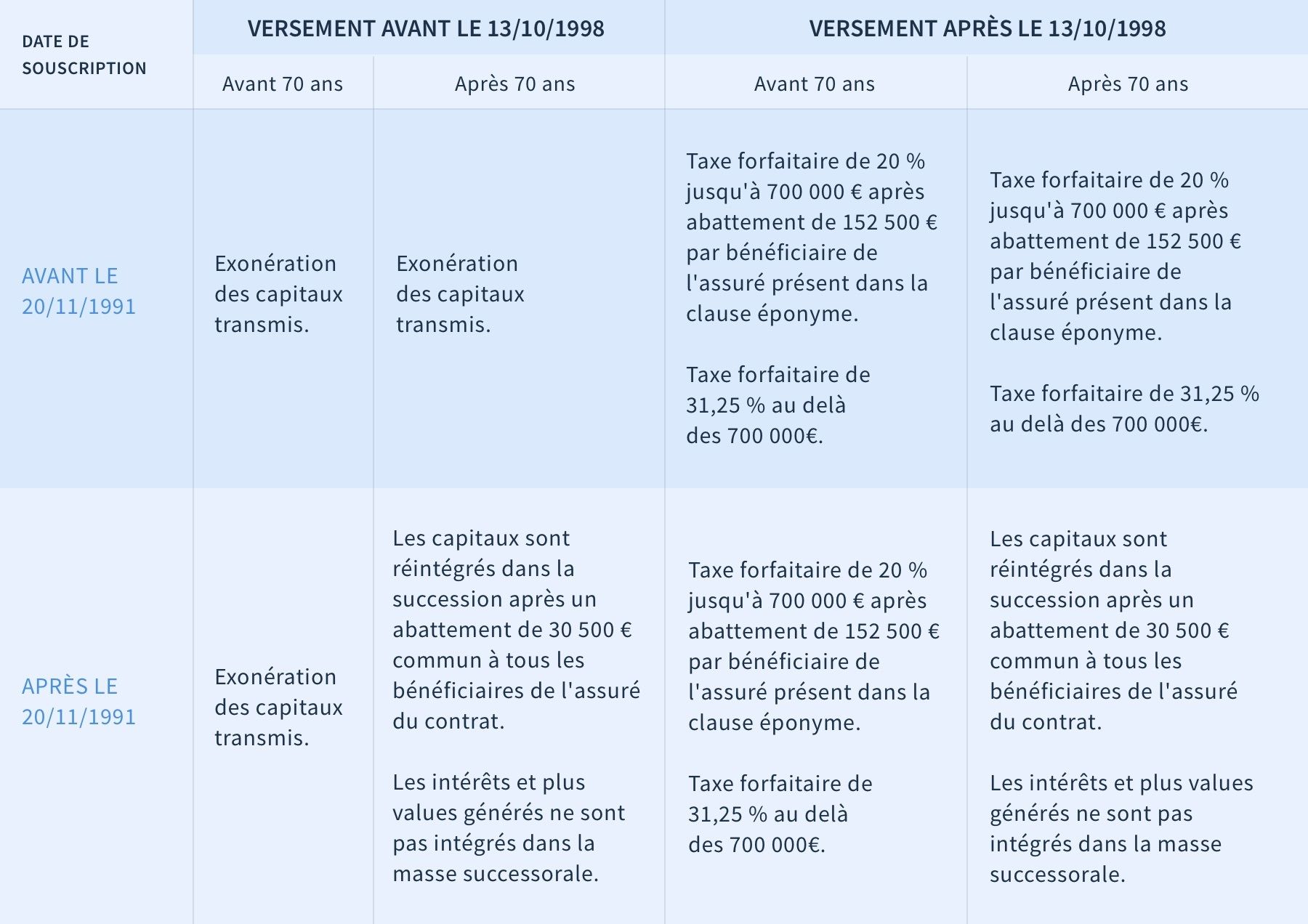

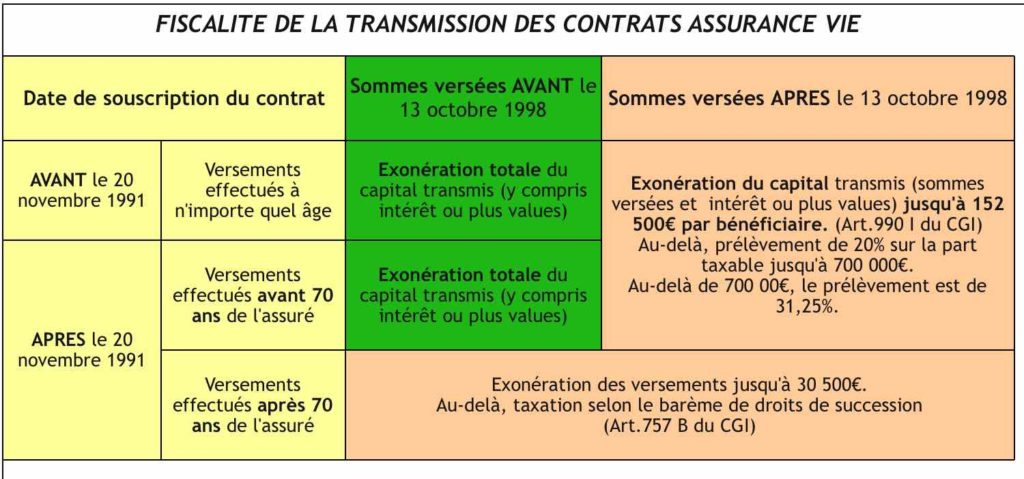

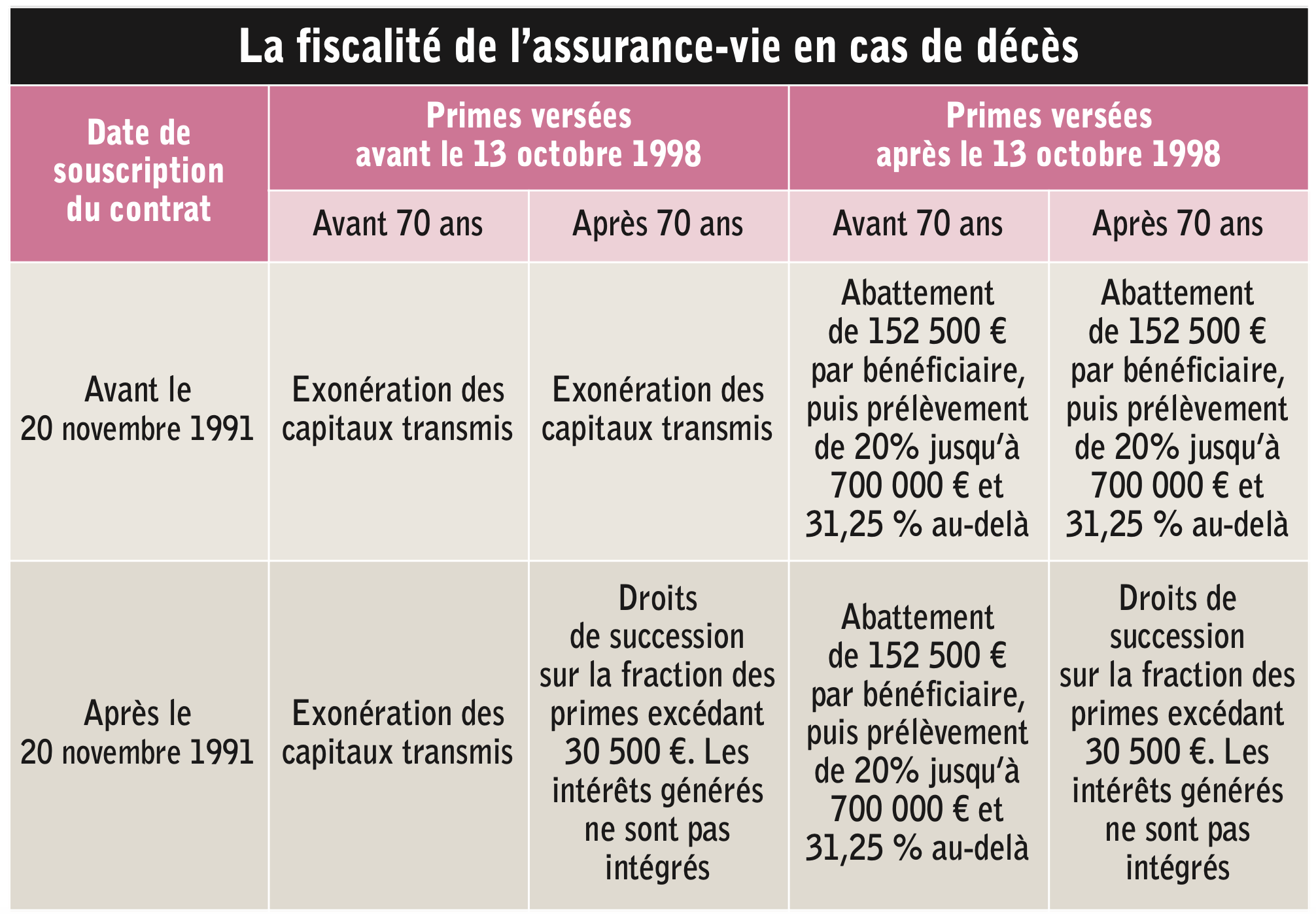

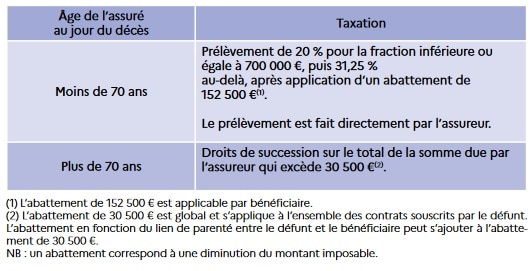

- The age of the deceased when the premiums were paid: This is a big one. Policies taken out before a certain age (typically 70) have different tax rules than those taken out later.

- The amount of the payout: Obviously, the more money you get, the more tax you might have to pay.

Specifically, for policies taken out after November 20, 1991, premiums paid before the deceased turned 70 are generally exempt from inheritance tax up to €152,500 per beneficiary. Premiums paid after 70 have a much lower exemption of only €30,500, which is shared among all beneficiaries.

See why it's so important to know when Aunt Ginette took out those policies? It can make a HUGE difference in the amount of tax you owe.

Where Do You File It?

The "Déclaration Partielle de Succession Pour Assurance Vie" is usually filed with the local tax office (service des impôts des entreprises, or SIE) where the deceased lived. Your notary (if you’re using one) will typically handle this, but it's still good to know where it goes.

Important: There are deadlines for filing this declaration, so don't procrastinate! (Unless you enjoy paying penalties, which I highly doubt.) The deadline is typically six months from the date of death.

Getting Help (Because You Probably Need It)

Let's be honest, navigating French inheritance law can be a nightmare. It's complicated, confusing, and full of loopholes and exceptions. That's why it's almost always a good idea to get professional help.

Consider consulting with:

- A Notary (Notaire): They are the experts in inheritance matters in France. They can guide you through the entire process, from gathering the necessary documents to filing the declaration and paying the taxes.

- A Tax Advisor (Conseiller Fiscal): They can help you understand the tax implications of the life insurance payouts and identify any potential exemptions or deductions.

- An Insurance Professional: Your insurance company can also provide information about the policy and the beneficiary payout.

My Aunt Ginette’s legacy was…complicated. But learning about this "Déclaration Partielle de Succession Pour Assurance Vie" at least made the process a little less daunting. And maybe, just maybe, it will help you too, should you ever find yourself swimming in a sea of inheritance paperwork. Good luck!

Final Thought: Don’t be afraid to ask questions. It’s better to be informed than to make costly mistakes. And remember, you’re not alone!