Okay, so picture this: I’m at a café, sipping my much-needed (and overpriced) latte, eavesdropping – purely accidentally, obviously – on the conversation next to me. A guy is practically tearing his hair out, talking about "creditors," "over-indebtedness," and something about a "recevabilité" something-something. My ears perked up. Over-indebtedness? Sounds familiar to half the population these days, amirite? Then I realized he was talking about the post-filing process after getting his debt relief application accepted. And I thought, "Hey, that's a topic many people need to understand better!" So, here we are. Let’s dive into what happens after your over-indebtedness application ("dossier de surendettement") has been deemed admissible ("recevable").

The Relief… And The (Slightly Less Intense) Stress

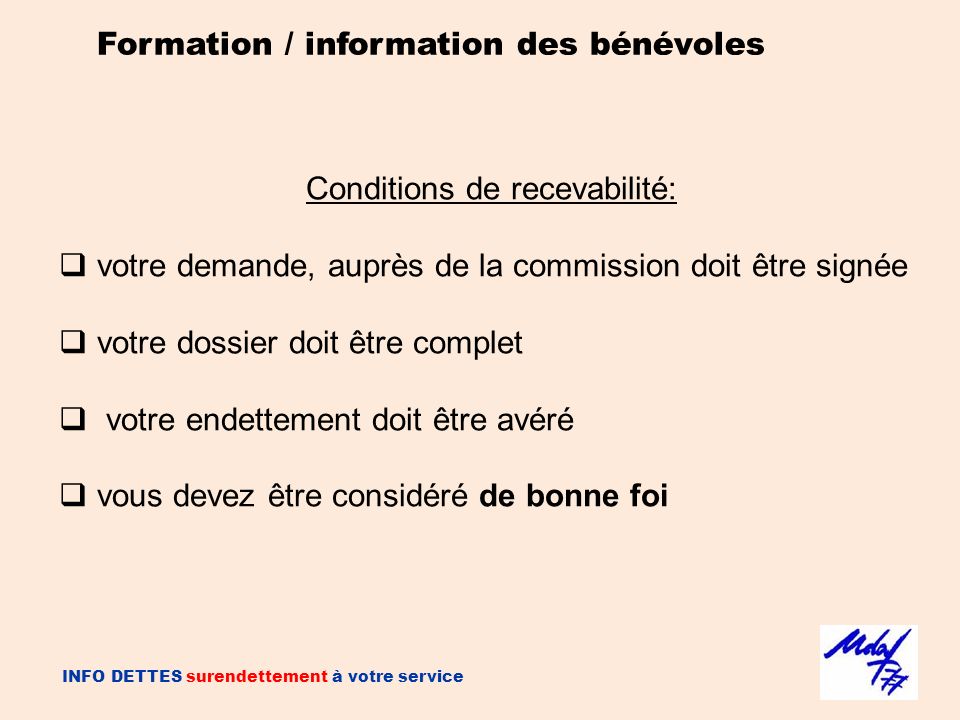

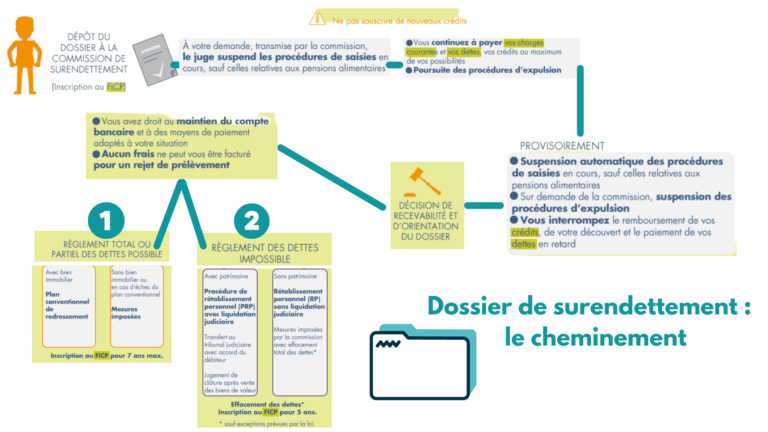

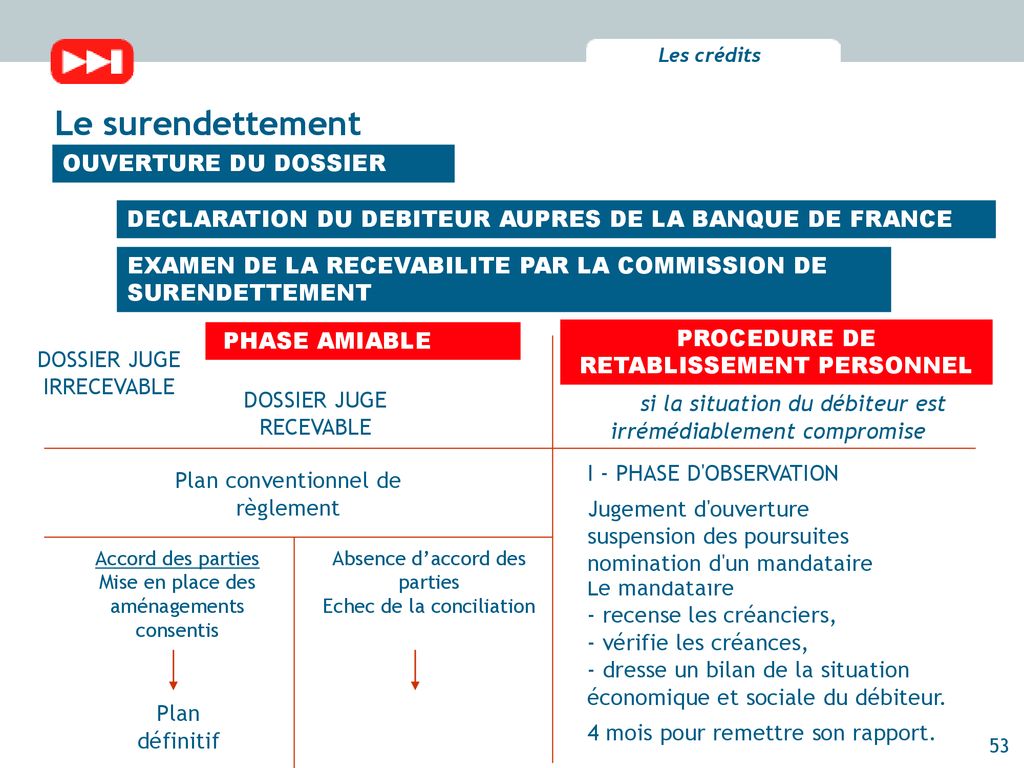

Getting your dossier de surendettement declared recevable is a HUGE weight off your shoulders. Seriously, it’s like winning a small lottery. The Commission de Surendettement (Over-Indebtedness Commission) has basically said, “Okay, we see you. We understand you're struggling. Let's try to figure this out." But – and there’s always a but, isn’t there? – it’s not over over. It’s just the start of the next phase. Think of it as graduating from pre-algebra to… slightly more complicated algebra. Still algebra, though.

One of the first things that happen after the recevabilité is declared is that your creditors get notified. And that's where things can get… interesting.

What Happens When The Creditors Get The News?

Alright, so the Commission sends a notification to all your creditors – banks, credit card companies, loan providers, even that one friend you owe 50€ to (okay, maybe not your friend, but you get the idea). This notification is a big deal for a few reasons:

- Suspension of Collections: Most importantly, it triggers a suspension of most collection proceedings. No more harassing phone calls (hopefully!), no more bailiffs knocking at your door (again, hopefully!), and no more legal actions aimed at seizing your assets. This is the immediate breathing room you desperately needed. A temporary truce, if you will.

- Inventory and Verification: Creditors are required to provide the Commission with a detailed list of what you owe them – the principal amount, interest rates, fees, etc. This is crucial for the Commission to get a clear picture of your total debt. Think of it as a financial x-ray.

- Opportunity to Challenge: Creditors also have the opportunity to dispute the admissibility of your dossier. They can argue that you don't meet the eligibility criteria for over-indebtedness, or that you intentionally created the debt situation. This is where things can get a bit… contentious.

Side note: don’t panic if a creditor challenges the recevabilité. It doesn't automatically mean your application will be rejected. The Commission will review the creditor's arguments and make a final decision.

The Creditor's Response: A Mixed Bag

Now, let's talk about how creditors might react. It's not always a smooth sailing situation, and knowing what to expect can help you navigate this phase with a little more… sanity. (Which, let's face it, you probably need by this point).

- Acceptance (Rare, but Possible): In some cases, creditors simply accept the Commission's decision and cooperate with the process. They understand that you're genuinely struggling and are willing to work towards a solution. This is the unicorn of debt relief scenarios.

- Passive Resistance: Some creditors might not actively challenge the recevabilité, but they might be slow to provide the required information or unresponsive to the Commission's requests. This can delay the process and create unnecessary frustration. (Pro tip: document everything. Every email, every phone call, every carrier pigeon message… okay, maybe not carrier pigeons.)

- Active Challenge: As mentioned earlier, some creditors will actively challenge the recevabilité. They might argue that you're not genuinely over-indebted, that you have hidden assets, or that you're simply trying to avoid paying your debts. This usually involves legal arguments and can require you to provide additional documentation to support your case.

- Debt Collection Agencies Step In: Be prepared for debt collection agencies to become more involved. Sometimes, the initial creditor might not challenge the recevabilité directly but sells your debt to a collection agency who will then make their claim.

The key is to stay informed and cooperate fully with the Commission. The more transparent and forthcoming you are, the better your chances of achieving a favorable outcome. It's also worth noting that the Commission has the power to impose sanctions on creditors who act in bad faith or refuse to cooperate.

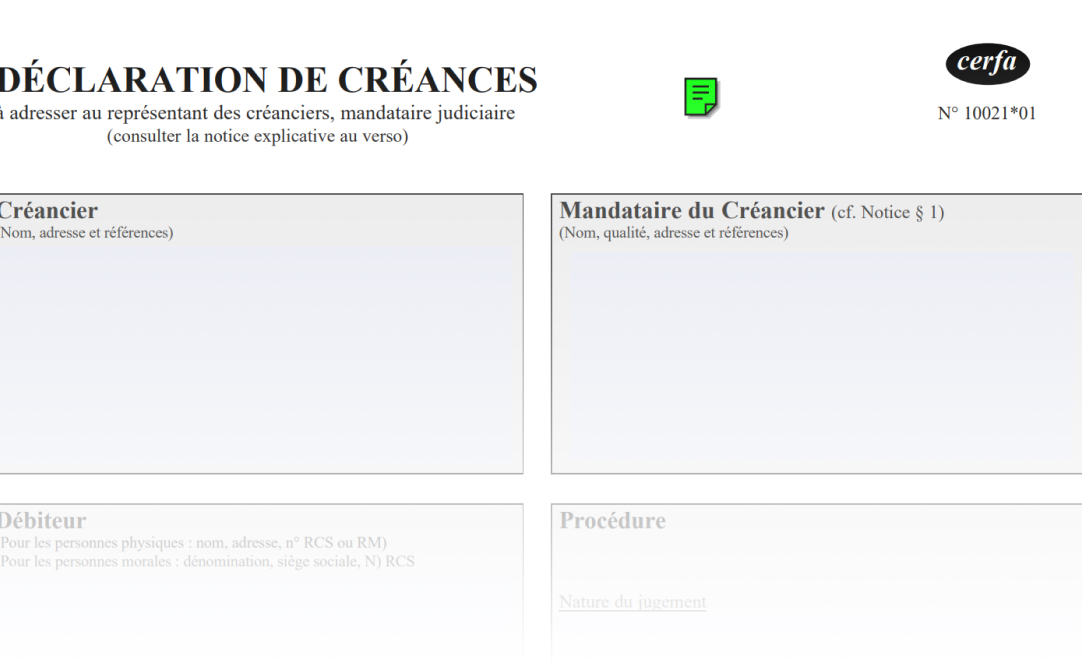

Navigating the "Declaration de Créances"

One of the most important things for you to do during this period is to carefully review the "Déclaration de Créances" (Declaration of Debt) submitted by each creditor. This document outlines the details of your debt, including the outstanding balance, interest rates, fees, and payment history.

%2C+y+compris+les+découverts+en+compte..jpg)

It's crucial to check these declarations for any errors or discrepancies. For example:

- Incorrect Balances: Make sure the outstanding balance matches your records. Sometimes, creditors make mistakes or include charges that you don't believe are valid.

- Incorrect Interest Rates: Verify that the interest rate is consistent with the terms of your original loan agreement.

- Unjustified Fees: Check for any fees that seem excessive or that you were not properly notified about.

- Statute of Limitations: Is some of the debt beyond the statute of limitations? If so, it may not be legally enforceable.

If you find any errors or discrepancies, notify the Commission immediately. You'll need to provide evidence to support your claims, such as copies of your loan agreements, payment statements, or any other relevant documentation. The Commission will then investigate the matter and make a determination.

Remember: Silence implies consent. If you don't challenge a creditor's declaration, the Commission will assume that you agree with the information provided. Don't let incorrect information sabotage your chances of a successful debt relief plan.

What to do if a Creditor Disputes the Admissibility?

Okay, so a creditor is being difficult. They've officially challenged the recevabilité of your dossier. What now? Don't panic! (Easier said than done, I know.) Here's a breakdown of what to expect and how to handle it:

- Review the Creditor's Arguments: Carefully read the creditor's reasons for challenging the recevabilité. Understand their concerns and identify any weaknesses in their arguments.

- Gather Evidence to Support Your Case: Collect any documents or information that support your claim of over-indebtedness. This might include pay stubs, bank statements, medical bills, or any other evidence that demonstrates your financial hardship.

- Seek Legal Advice (Optional but Recommended): Consider consulting with a lawyer specializing in debt relief. They can help you understand your rights and options, and represent you in negotiations with the creditor. While not compulsory, it might be a good investment given the legal complexities.

- Communicate with the Commission: Keep the Commission informed of any developments in the case. Provide them with any new evidence or arguments that support your position.

- Attend Hearings (If Necessary): In some cases, the Commission may hold a hearing to gather more information and hear arguments from both sides. Be prepared to present your case clearly and concisely.

The Commission will ultimately make a decision based on the evidence presented. If they uphold the recevabilité, the process will continue. If they reject it, you may have the option to appeal the decision to the courts. It's a legal minefield, so that lawyer is looking more and more attractive right now, right?

The End Goal: A Debt Relief Plan

All of this – the creditor notifications, the declarations of debt, the potential challenges – it all leads to one thing: the creation of a debt relief plan. The Commission will work with you and your creditors to develop a plan that is both feasible for you and acceptable to your creditors. (That's the idea, anyway.)

The plan might involve:

- Debt Consolidation: Combining all your debts into a single loan with a lower interest rate.

- Debt Reduction: Negotiating with creditors to reduce the amount you owe.

- Payment Moratorium: Temporarily suspending your debt payments.

- Debt Repayment Schedule: Establishing a structured payment plan to repay your debts over a longer period.

Once the plan is agreed upon (either amicably or imposed by the Commission), you'll need to stick to it religiously. Failure to comply with the terms of the plan can lead to its termination and the resumption of collection proceedings. Think of it like a marathon, not a sprint. It takes discipline and perseverance to reach the finish line. And maybe a good sports drink. Or two. Or five.

The appel des créanciers after the recevabilité of your dossier de surendettement is a critical stage. It requires vigilance, cooperation, and a healthy dose of patience. But remember, you're not alone in this. The Commission is there to help you, and there are resources available to provide you with legal and financial guidance. Stay strong, stay informed, and remember that financial freedom is within reach.

+©.jpg)

+©.jpg)